What You Need to Know About Savings Groups

A savings group is a community-based way for people to save money, access loans, and support each other financially. Learn how you can join or start a group today.

What is a Savings Group?

A Savings Group brings together 10 to 20 people from the community. These members save money, borrow, and manage their finances as a team. Each person contributes a set amount every week or month. As a result, the group builds a shared pool of funds.

Members can take loans from this pool for different needs. Because of this, they enjoy better access to credit and more financial freedom. Savings Groups help people build good money habits and become more self-reliant. In addition, they offer strong social support, especially in low-income or underserved areas.

You can join a Savings Group to save money, get loans, and improve your financial stability. At the same time, you will strengthen community bonds and learn more about managing money. Furthermore, Savings Groups support discipleship, church planting, and Pioneer Business Planting. This creates a complete approach to community development.

Advantages of a Savings Group

Financial Inclusion: Savings Groups provide access to financial services for individuals who may not have access to traditional banks or financial institutions, promoting financial inclusion and economic empowerment.

Savings and Asset Building: Members can save money regularly, allowing them to accumulate savings for emergencies, investments, or personal goals, ultimately improving their financial stability.

Access to Credit: Savings Groups offer members the opportunity to borrow from the group’s savings pool at lower interest rates than those offered by moneylenders, helping members meet immediate financial needs.

Community Support: These groups foster a sense of community and mutual support, as members work together to achieve their financial goals and solve financial challenges collectively.

Financial Literacy: Together with our Pioneer Business Planting training, Savings Groups provide financial education and training, enhancing members’ financial knowledge and management skills, which can benefit them and their families in the long term.

How to Start a Savings Group

Starting a savings group is simple and empowering. Here’s how you can begin:

- Gather Members: Bring together 10–20 trusted people from your community who are interested in saving and supporting each other.

Set Group Rules: Decide together on the amount to save, meeting frequency, and basic rules for borrowing and repayments.

Elect Leaders: Choose a President, Treasurer, and Secretary to help manage the group’s activities and finances.

Open a Group Account or Use a Money Box: Keep the group’s savings secure in a bank account, mobile wallet, or a locked money box.

Hold Regular Meetings: Meet weekly or monthly to collect savings, review loans, and support each other.

Keep Transparent Records: Use passbooks or simple ledgers to track everyone’s savings, loans, and repayments.

Review and Celebrate: At the end of each cycle, share out the savings and celebrate your achievements together!

Organizational Structures of Savings Groups

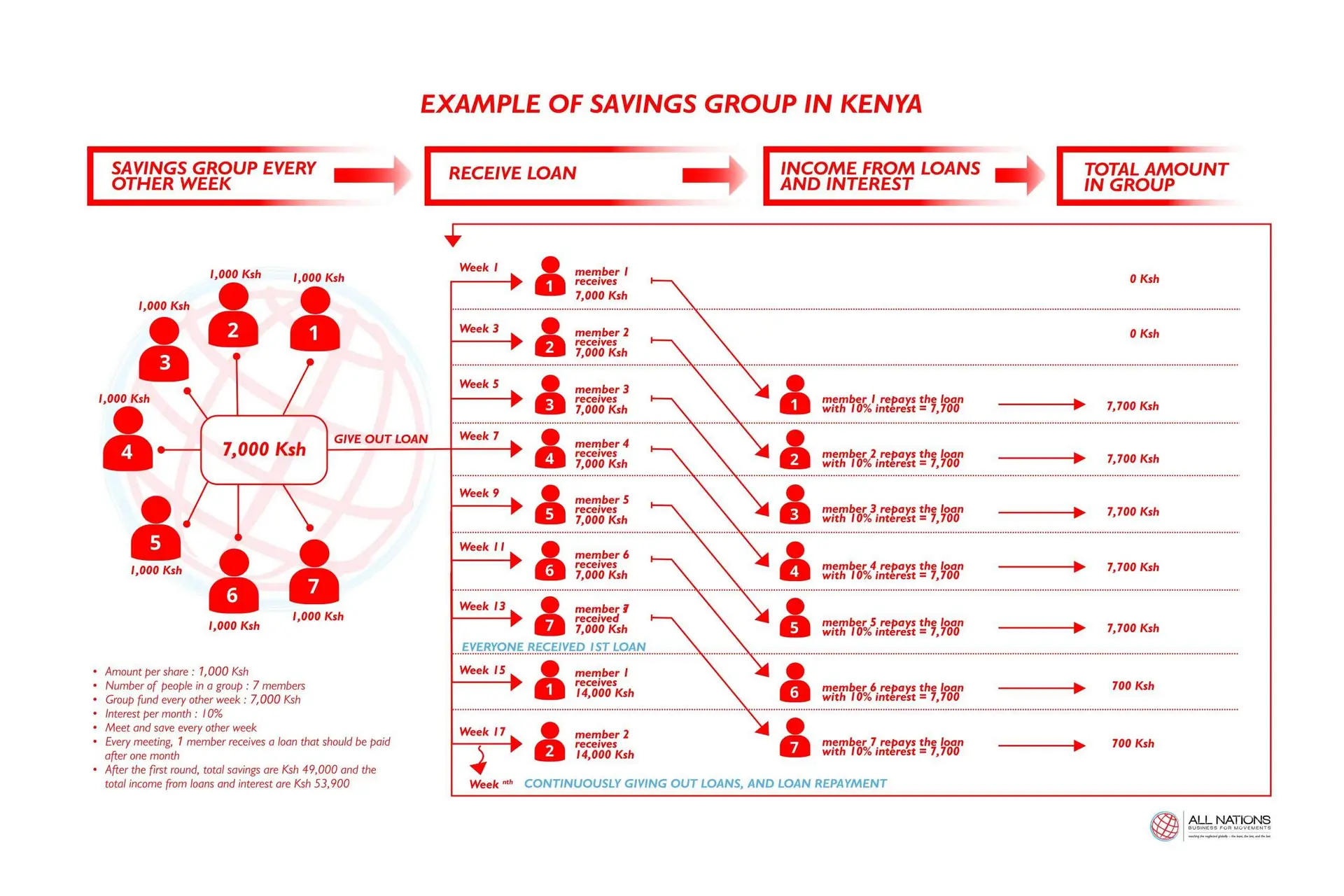

- Normal Savings Group: A normal savings group usually includes 10 to 25 people, but sometimes up to 50. Members meet every week to buy shares. Each person can buy between one and five shares, and the price stays the same for the whole cycle. Members can choose how much to save. The group holds elections to pick leaders, such as a President, Treasurer, and Secretary. This ensures everyone is fairly represented.

- Loans: The group creates a loan fund. Members can borrow up to three times the amount they have saved. They must repay loans within three months. Unlike formal Micro Finance Institutions (MFIs), these groups offer flexible repayment options.

- Social Fund: Many groups set up a social fund, which acts like simple insurance. Members add a small amount at each meeting. If someone faces an emergency, they can use this fund for help.

- Share-outs: At the end of each cycle, everyone repays their loans. Then, the group shares out all the savings, interest, and fines based on how much each person saved. Members can reinvest their share, which helps them qualify for bigger loans in the next cycle.

- Record-keeping and Finances: The group keeps its money safe in a bank account, mobile wallet, or money box. They use passbooks and cash records to track everything. This way, everyone can trust the process and see where the money goes.

- Table Banking: Table banking is another way to run a savings group. Here, at least five people contribute a set amount regularly. The group gives all the collected money to one member to start or grow a business. Over time, every member gets a turn to receive the funds. Usually, the group reviews a written business plan before choosing who gets the money next. Unlike normal savings groups, table banking does not have share-outs at the end of the cycle.